PSTAT 100: Lecture 13

Examples of Statistical Modeling

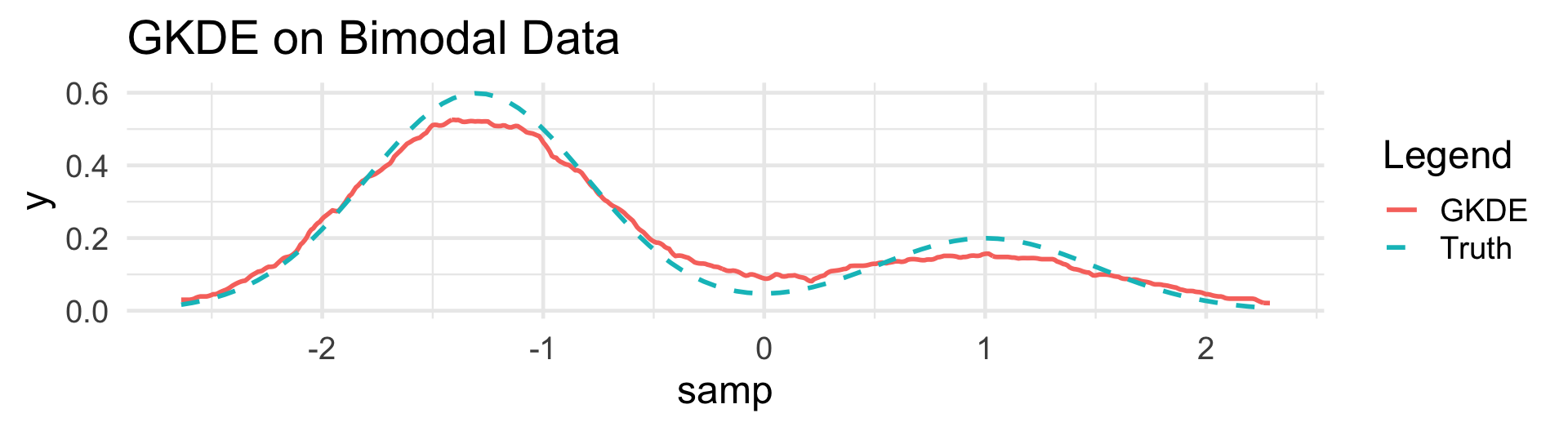

Density Estimation

Framework

Data: A collection of numerical values; \(\vect{x} = (x_1, \cdots, x_n)\) we believe to be a realization of an i.i.d. random sample \(\vect{X} = (X_1, \cdots, X_n)\) taken from a distribution with density f().

Goal: to estimate the true value of f() at each point.

Histograms, Revisited

Histograms, Revisited

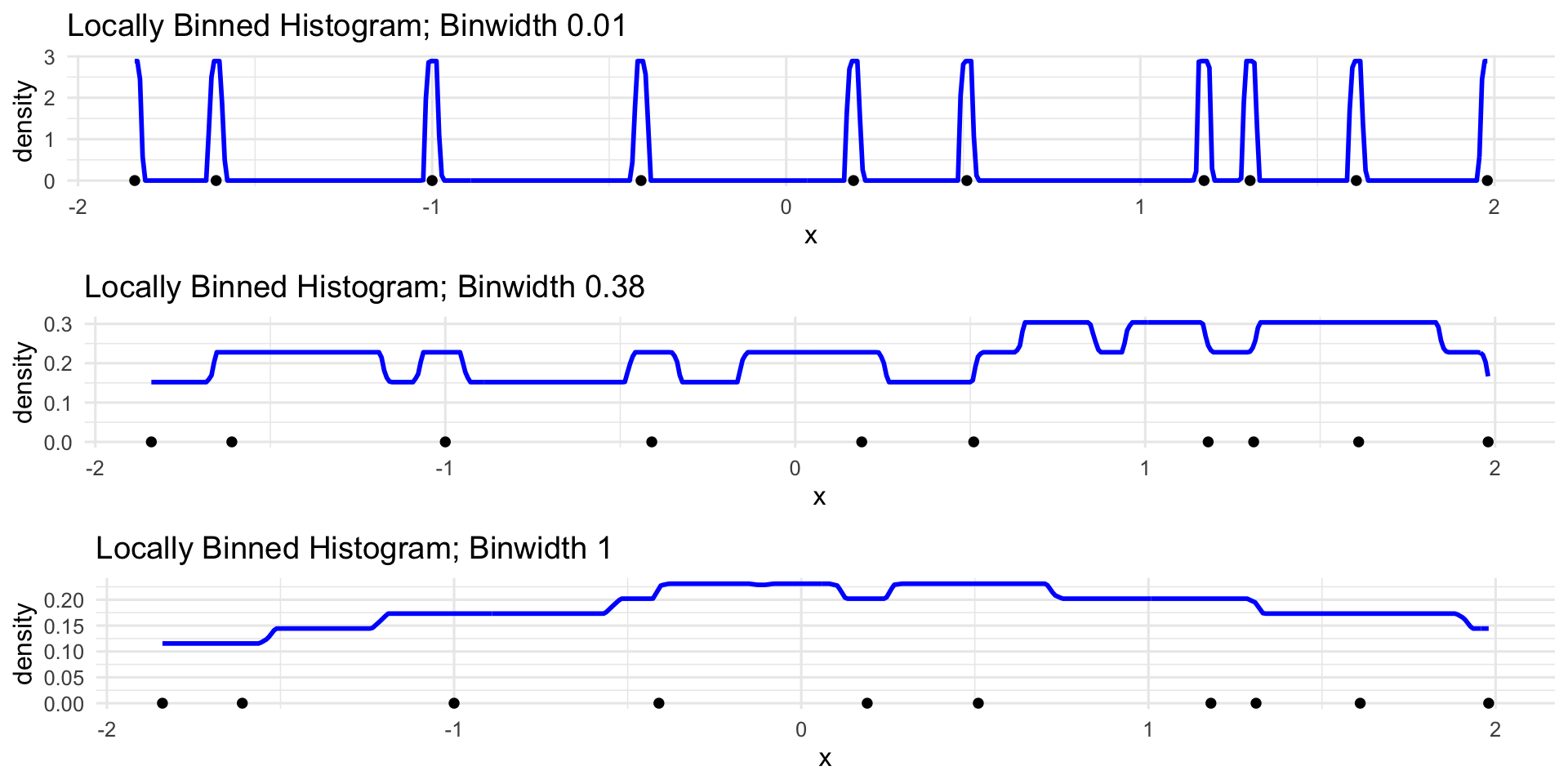

Local Binning

\[ \widehat{f}_{\mathrm{lb}}(x) = \frac{1}{nh} \sum_{i=1}^{n} 1 \! \! 1_{\{ \left| x_i - x \right| < \frac{h}{2} \}} \]

Histograms, Revisited

Local Binning

Histograms, Revisited

Local Binning

\[ \widehat{f}_{\mathrm{lb}}(x) = \frac{1}{n} \sum_{i=1}^{n} \left[ \frac{1}{h} 1 \! \! 1_{\{ \left| x_i - x \right| < \frac{h}{2} \}} \right] \]

- Changing xi amounts to changing the “center” of the “box”

- Changing h amounts to changing the width and height of the “box”

- Note, however, that for any value of h and xi, the area underneath this graph is always 1.

- Nonnegative function that integrates to one…

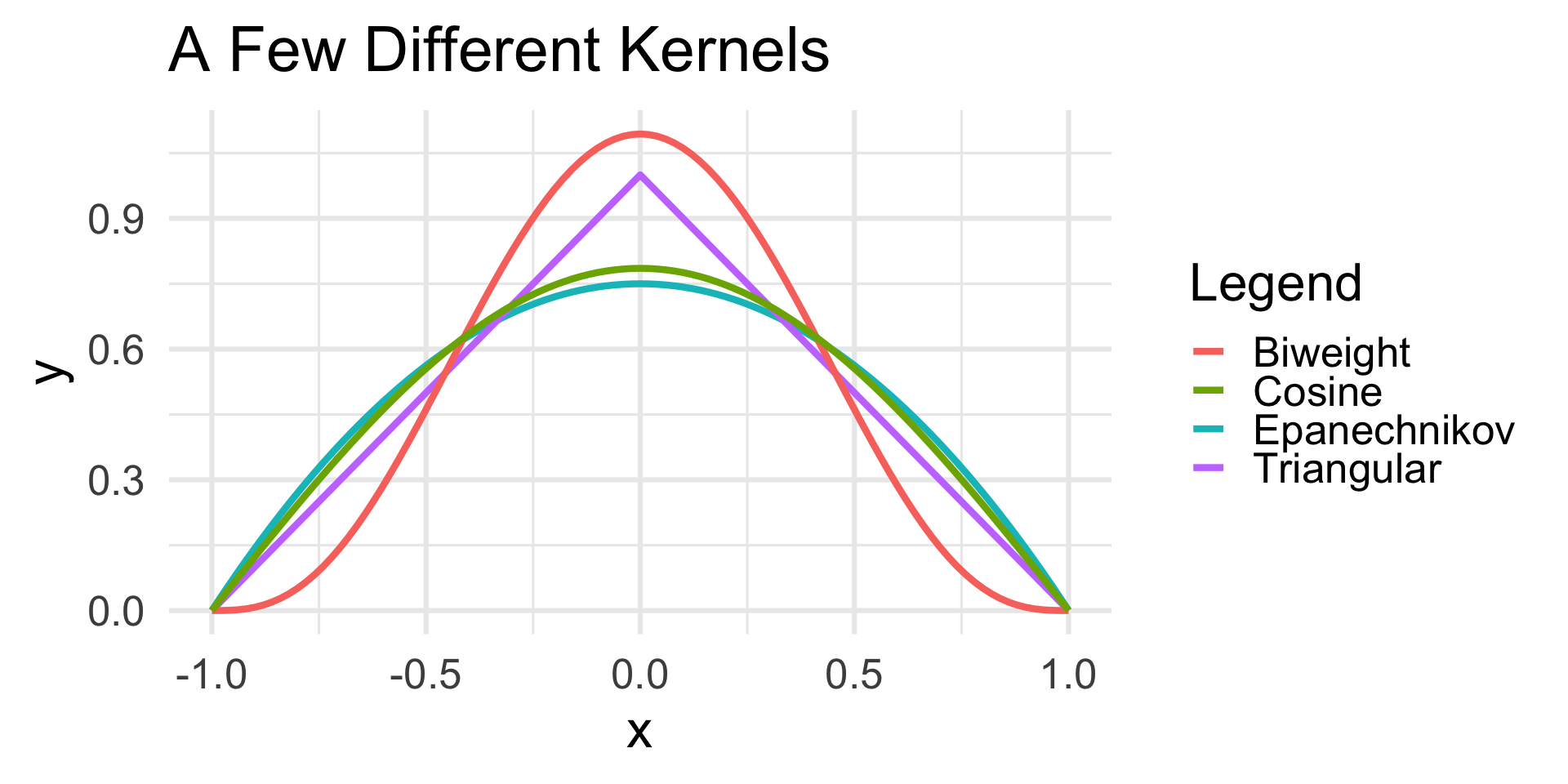

Kernel Density Estimation

Kernels

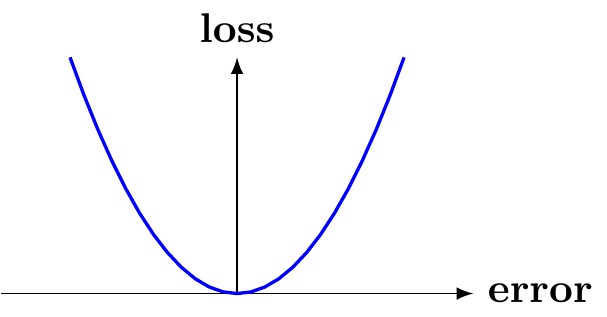

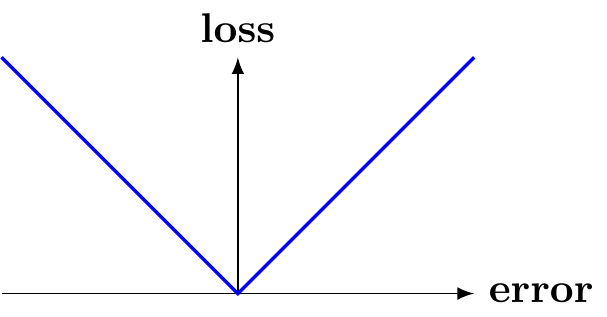

Loss Functions

There are many choices for loss functions, each with pros and cons.

For numerical data, the two most common loss functions are:

Squared Error (aka L2)

\(\mathcal{L}(y_i, \theta) = (y_i - \theta)^2\)

Absolute Error (aka L1)

\(\mathcal{L}(y_i, \theta) = |y_i - \theta|\)

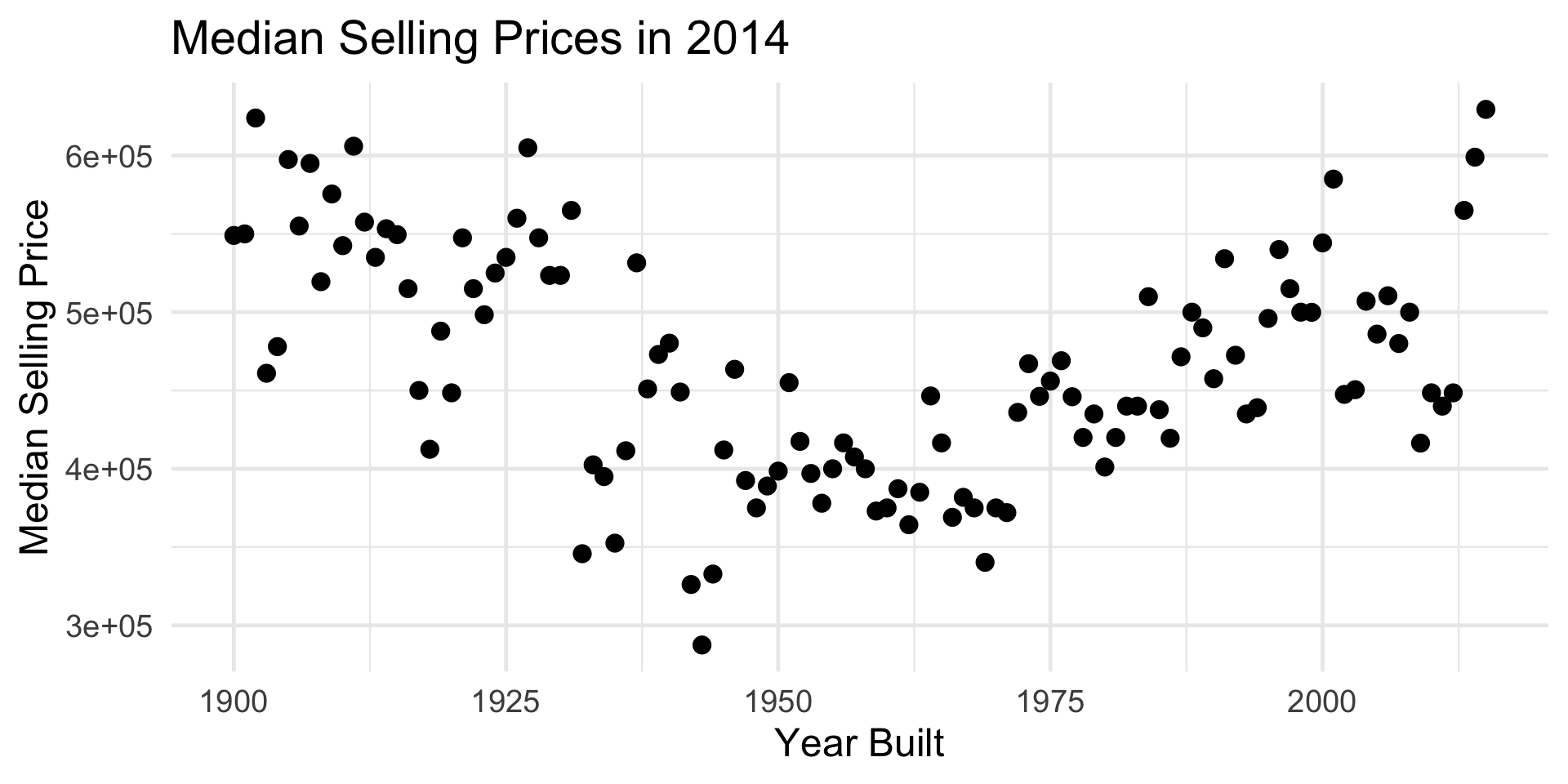

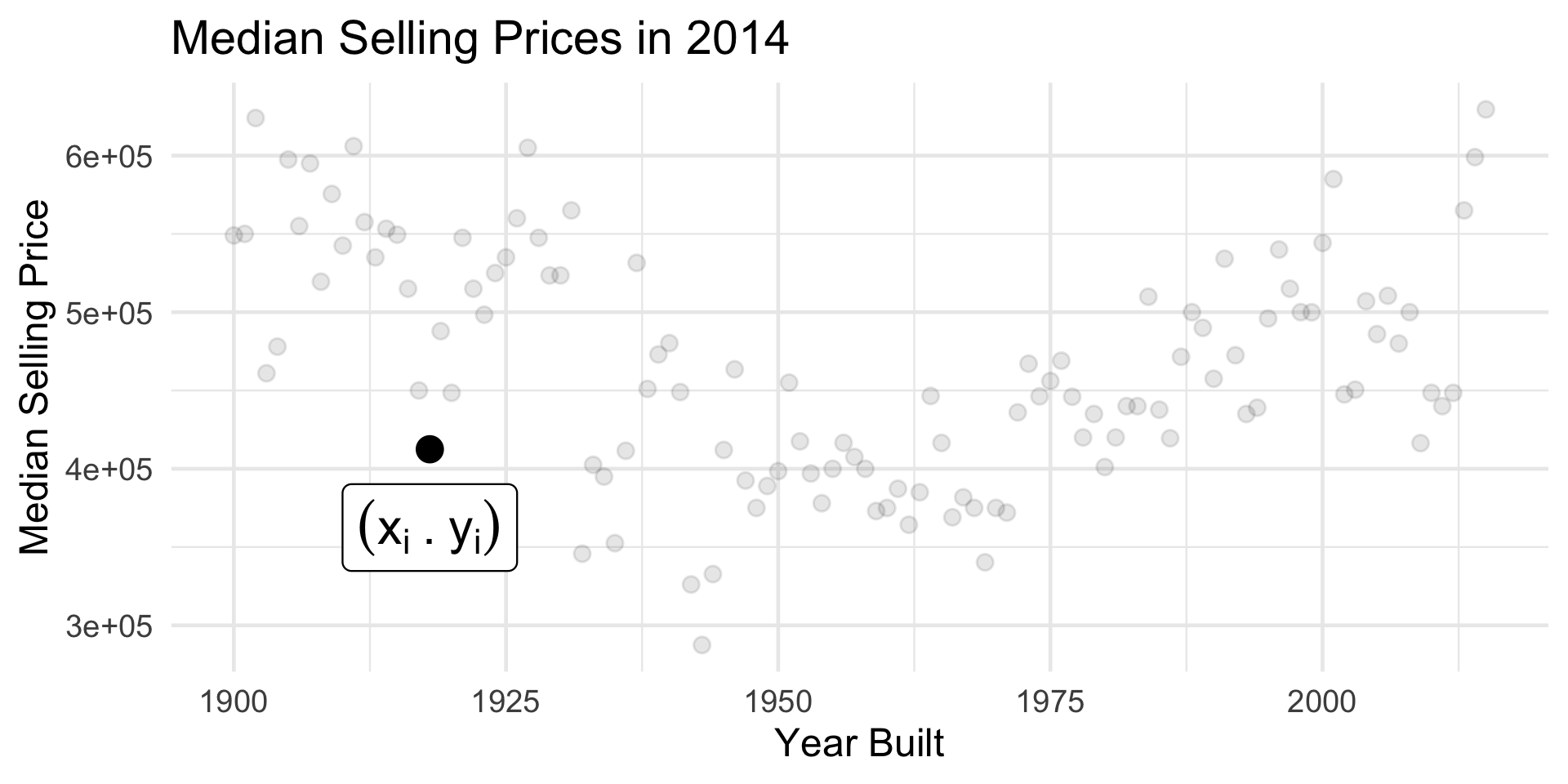

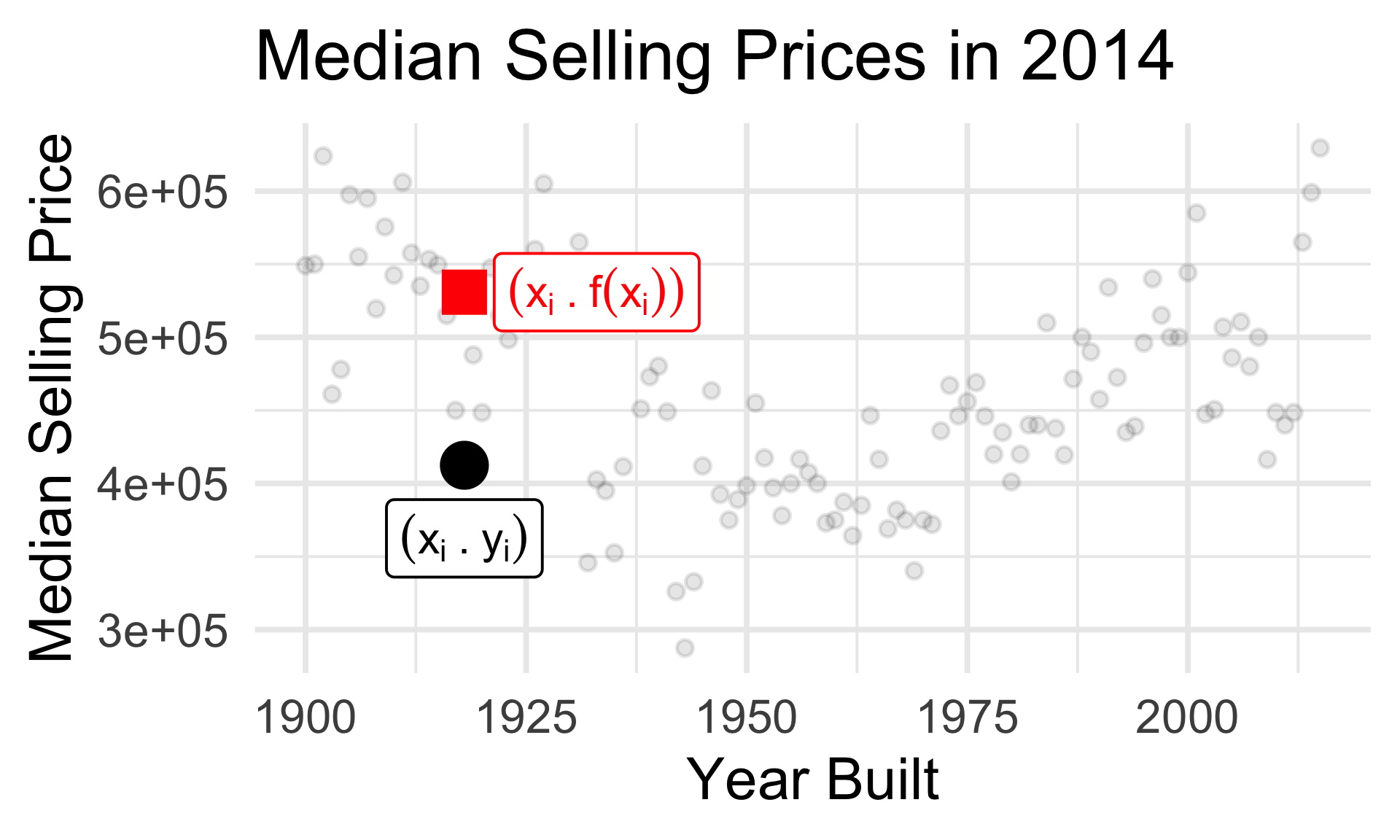

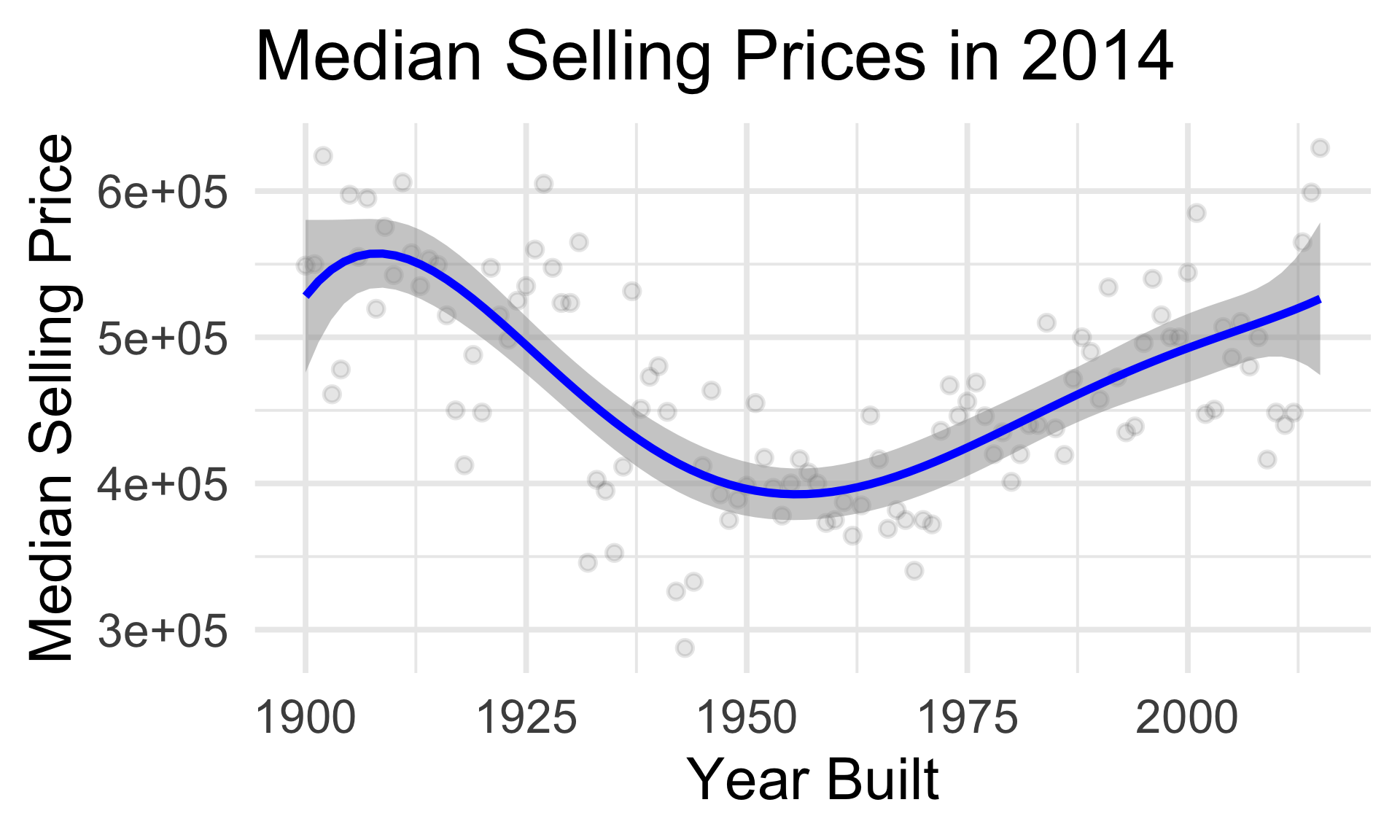

Housing Data

An Example

Housing Data

Building a Model

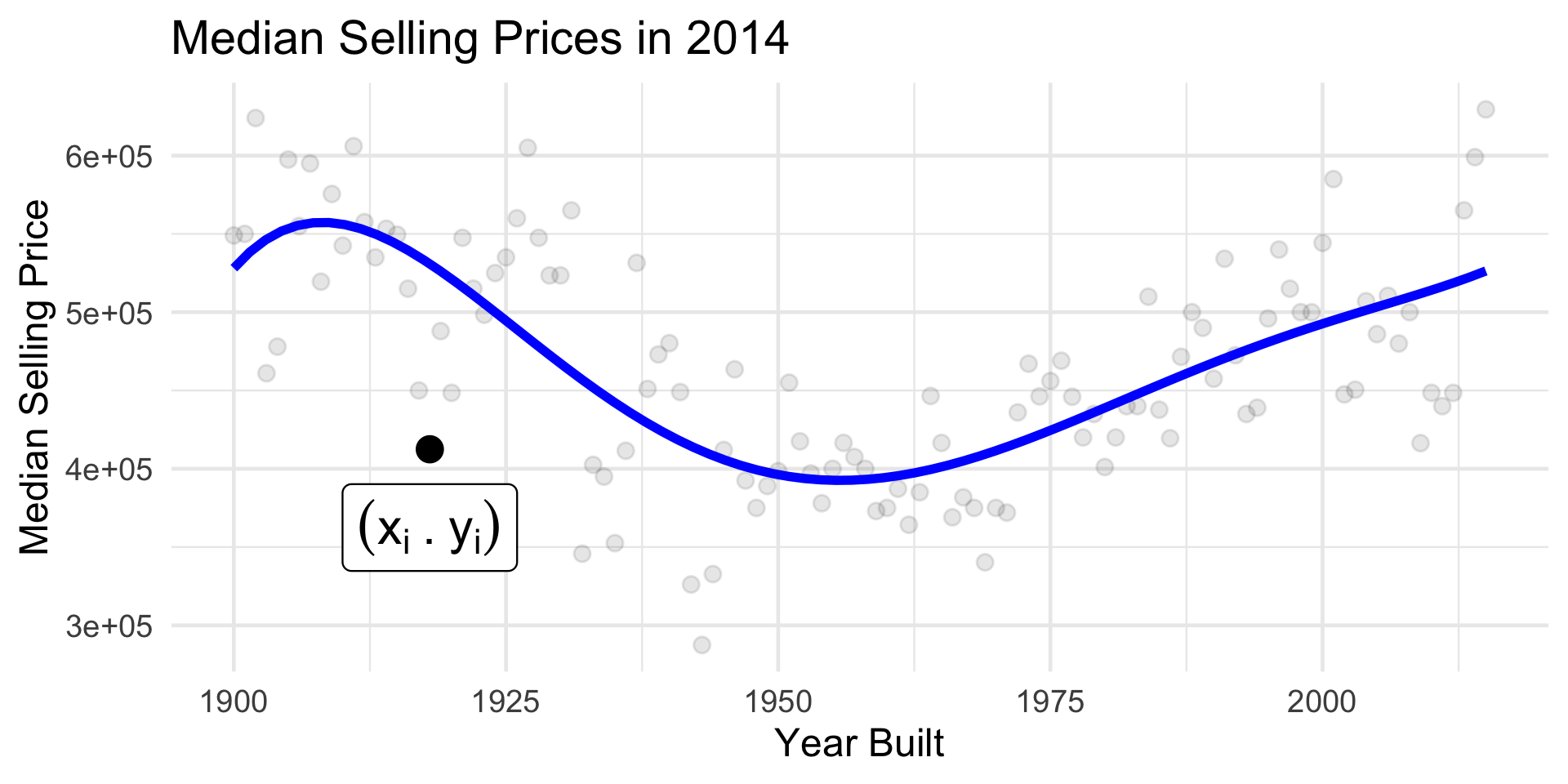

Housing Data

Building a Model

Housing Data

Building a Model

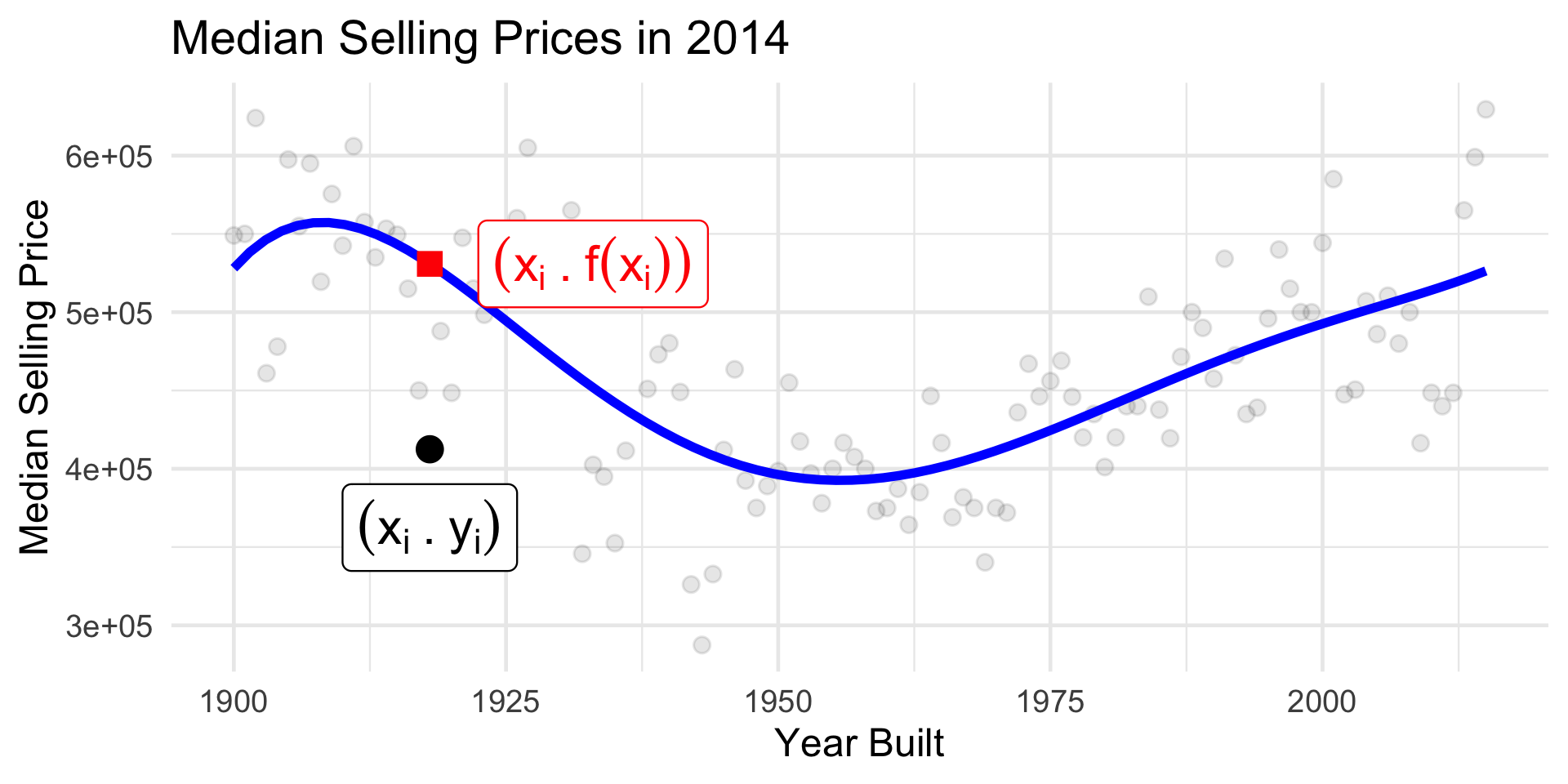

Housing Data

Building a Model

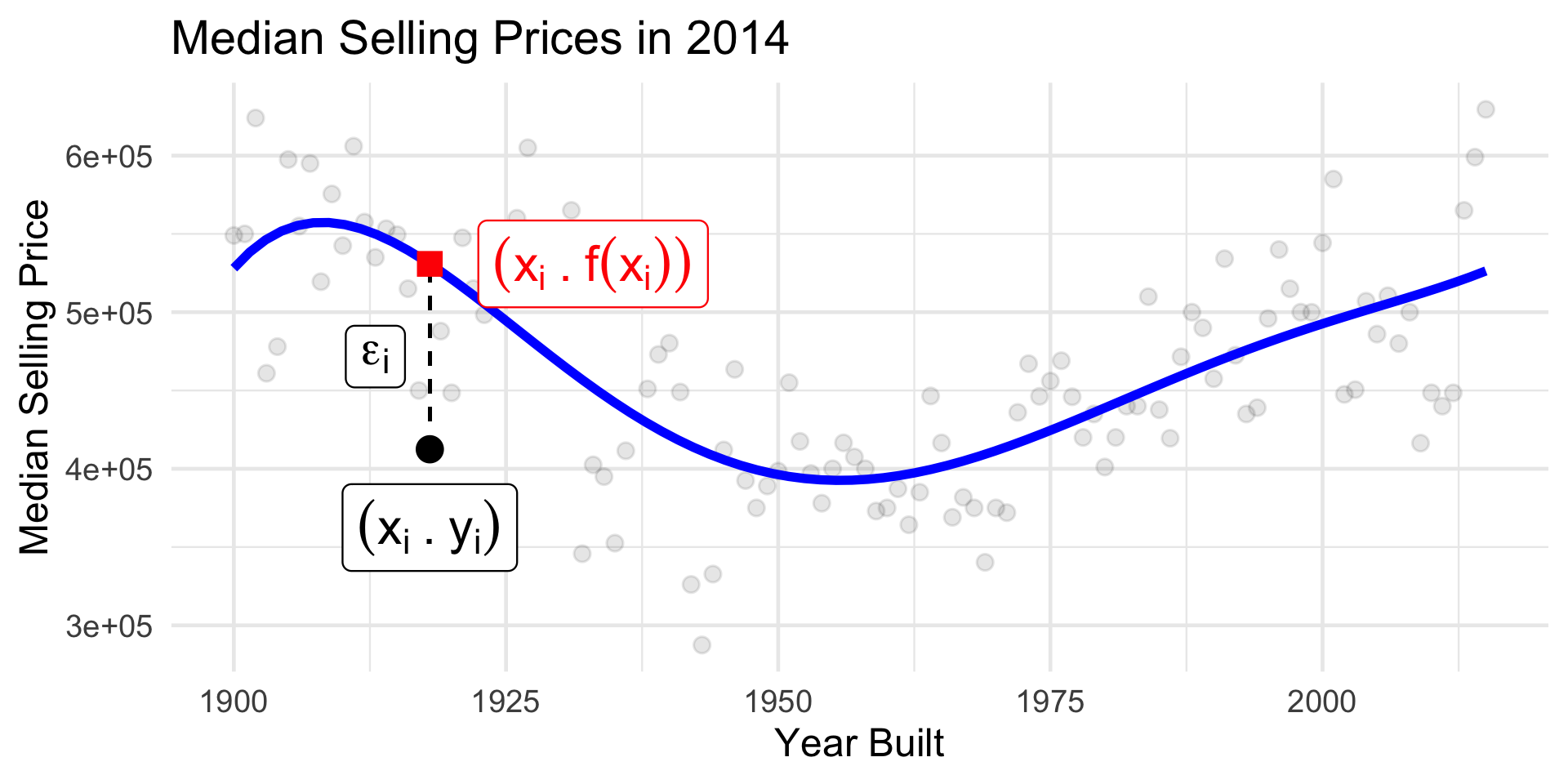

Why Model?

Prediction

- What’s the true (de-noised) median selling price of a house built in 1918?

Inference

- How confident are we in our guess about the relationship between year built and selling price?